GST Audit in India: A Comprehensive Guide

I. Introduction

The Goods and Services Tax (GST) regime, implemented in India in July 2017, was a landmark shift in the country’s indirect tax framework. It replaced a host of central and state taxes with a unified structure, aimed at increasing transparency, improving ease of doing business, and streamlining tax administration. However, with such a broad tax base and numerous compliance requirements, maintaining oversight is critical. This is where GST audits come into play.

A GST audit is a formal examination of a taxpayer’s financial records, returns, and other documents to ensure that the taxes declared, paid, and claimed under the GST law are accurate and compliant. The audit aims to verify the correctness of key financial elements such as turnover, input tax credit (ITC), refunds claimed, and taxes paid, based on the provisions of the Central Goods and Services Tax (CGST) Act and associated rules.

The importance of GST audit lies not just in revenue protection, but also in promoting accountability among businesses. A well-conducted audit enhances trust in the tax system, detects errors or misreporting early, and encourages voluntary compliance.

In India, not all taxpayers are subject to an audit automatically. A GST audit may be triggered under specific conditions:

- On the recommendation or discretion of tax authorities.

- If there are discrepancies in returns or suspected revenue leakage.

- In cases involving complex transactions, significant refunds, or high turnover.

Understanding the audit mechanism is essential for all registered taxpayers to ensure smooth operations, avoid penalties, and demonstrate compliance in a transparent manner.

II. Types of GST Audit

Under the GST regime, there are two main types of audits, each governed by a distinct section of the CGST Act:

A. Departmental Audit (Section 65)

A Departmental Audit is initiated by tax authorities when they believe it is necessary to verify the accuracy of the returns and related records submitted by a taxpayer. It can be triggered based on risk assessments, inconsistencies in filings, or random sampling.

Procedure:

- The taxpayer receives a formal notice in Form GST ADT-01 at least 15 days before the start of the audit.

- The audit may be conducted either at the taxpayer’s business premises or at the office of the tax department.

- Tax officers have the authority to review books of accounts, returns, invoices, ITC claims, and refund details.

- The audit must be completed within three months, extendable by another six months under special circumstances.

Upon completion, a Final Audit Report is issued in Form GST ADT-02, summarizing the findings.

B. Special Audit (Section 66)

A Special Audit is more detailed and is usually ordered when the tax authorities believe that the nature of transactions is complex or there is a significant discrepancy in the reported turnover, input tax credit, or valuation of goods/services.

Key aspects:

- Initiated only upon the direction of the Commissioner.

- Conducted by a Chartered Accountant (CA) or Cost Accountant (CMA) who is nominated by the Commissioner, not chosen by the taxpayer.

- The auditor may request any records, explanations, or clarifications deemed necessary.

The findings of the special audit can lead to further proceedings, such as assessment or penalty, based on the conclusions drawn.

How it differs from a Departmental Audit:

- Departmental audits are routine and part of the general verification process.

- Special audits are exceptional in nature, conducted only when complexity or risk warrants a deeper financial inspection by a qualified external professional.

Understanding both types of audits is essential for businesses to prepare in advance and ensure that their GST filings and records are in strict compliance with applicable regulations.

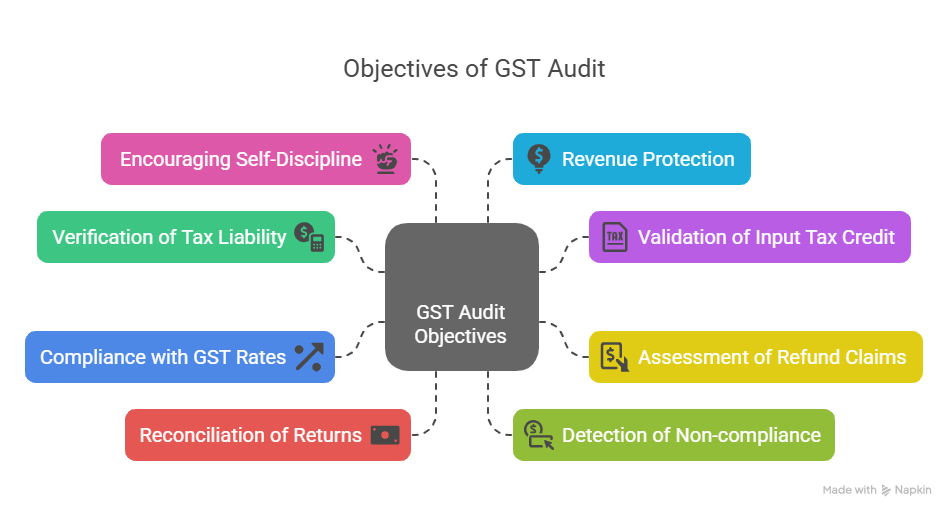

III. Objectives of GST Audit

The primary objective of a GST audit is to promote accuracy, transparency, and consistency in tax compliance. The Goods and Services Tax is a self-assessed regime, and while this facilitates ease of doing business, it also places significant responsibility on taxpayers to file correct and complete information. An audit serves as a checkpoint to ensure this responsibility is being met.

Below are the key objectives of conducting a GST audit:

1. Verification of Tax Liability

The audit examines whether the taxpayer has correctly determined and paid their GST liability. This involves checking turnover, tax invoices, outward supplies, and whether the correct rate of GST has been applied as per the applicable law.

2. Validation of Input Tax Credit (ITC)

Since ITC is a cornerstone of the GST system ensuring it is claimed in accordance with law is critical. Auditors scrutinize ITC records to verify eligibility, matching with GSTR-2A/2B, and ensure that the credit has not been availed on restricted or blocked inputs.

3. Assessment of Refund Claims

Refunds, particularly in export-driven or inverted duty structure businesses, are another key area of review. The audit checks whether the refund claimed is accurate, supported by relevant documentation, and free from duplication or misreporting.

4. Compliance with GST Rates and Valuation Rules

The auditor assesses if the taxpayer has applied correct tax rates based on HSN/SAC classification, and whether the valuation of goods and services follows GST guidelines. Any misclassification or undervaluation could lead to short payment of taxes.

5. Reconciliation of Returns and Financial Statements

Cross-verification of GST returns (GSTR-1, GSTR-3B, GSTR-9) with the books of accounts is a critical objective. The auditor ensures consistency between what is filed and what is recorded in the financials, minimizing the scope of manipulation or omission.

6. Detection of Non-compliance and Fraud

One of the most important objectives of a GST audit is to detect anomalies, if any, that could indicate tax evasion or manipulation. These could include misreporting of exempt supplies, non-reversal of ineligible ITC, or inflated input claims.

7. Encouraging Self-Discipline Among Taxpayers

The audit mechanism also has a preventive objective: to encourage businesses to follow proper compliance procedures and maintain accurate records. The prospect of being audited ensures that taxpayers stay vigilant and adopt best practices.

8. Revenue Protection and Policy Feedback

Audits help the government identify areas where revenue leakage is possible and provide valuable feedback for policy updates, sectoral risks, and system improvements.

IV. GST Audit Process: Step-by-Step

The GST audit process is methodically structured to ensure transparency, thorough examination, and fairness. Whether conducted by departmental authorities or by a nominated auditor in special cases, the audit process under GST follows defined procedures under the CGST Act and Rules.

Let’s break down the audit process into five key stages:

1. Intimation of Audit

- The audit process officially begins with an intimation notice to the taxpayer.

- In the case of a Departmental Audit under Section 65, the notice is sent using Form GST ADT-01, and it must be issued at least 15 working days prior to the commencement of the audit.

- The notice specifies the scope, period, and documents to be submitted or made available.

Key takeaway: A well-prepared taxpayer can reduce delays and scrutiny by organizing books and documentation as soon as notice is received.

2. Predictable Financial Planning

- The audit is conducted either at the taxpayer’s place of business or at the tax office.

- Officers (or auditors, in the case of a special audit) will begin by requesting access to books of accounts, GST returns, reconciliations, invoices, agreements, and any supporting evidence required for examination.

- The taxpayer must offer full cooperation, ensuring timely availability of information and staff.

Note: Refusing to cooperate or providing incomplete records may lead to further action under GST laws.

3. Verification and Examination

This is the core phase of the audit where intensive scrutiny takes place. Auditors examine:

- Turnover and outward supplies as declared in returns versus financial statements.

- GST rate application, exemptions claimed, and HSN code classification.

- Input Tax Credit (ITC) – eligibility, reversals, mismatches, and utilization.

- Refunds claimed and corresponding export documentation, where applicable.

- Tax payment timelines and any instances of delayed payment or short payment.

All these elements are cross-referenced with returns such as GSTR-1, GSTR-3B, GSTR-9, and books of account, to identify mismatches or gaps.

4. Completion and Reporting

- The audit must be completed within 3 months from the commencement date. However, the Commissioner may extend it by an additional 6 months in certain cases.

- A preliminary discussion is typically held with the taxpayer to communicate observations.

- The audit findings are then compiled into the Final Audit Report (Form GST ADT-02), which must be issued within 30 days of audit completion.

Important: This report will highlight discrepancies, if any, and form the basis for further legal action if required.

5. Post-Audit Actions

Based on the findings:

- If no discrepancies are found, the audit is formally closed without any further action.

- If discrepancies are found (e.g., under-reported turnover, ineligible ITC, excess refund), the taxpayer may be served a Show Cause Notice under Section 73 or 74, depending on whether fraud or willful misstatement is suspected.

The taxpayer is given a chance to explain or rectify issues. If accepted, payment of differential tax, interest, and penalties (if applicable) must follow.

By understanding each stage of the GST audit process, businesses can be better prepared, reduce their compliance burden, and avoid potential litigation or financial liability.

V. GST Audit Checklist

A successful GST audit is not only about responding to the department’s queries but also about internal preparedness. Below is a structured checklist that Indian businesses should follow to ensure accuracy, compliance, and transparency:

1. GST Return Reconciliation

- Reconcile GSTR-3B with GSTR-1 to verify outward tax liability.

- Match GSTR-3B with GSTR-2A or GSTR-2B to confirm eligible input tax credit (ITC).

- Cross-verify annual returns (GSTR-9 and GSTR-9C) with audited financial statements.

2. Invoice Compliance

- Ensure invoice formats meet GST requirements under Rule 46.

- Check that invoices include all mandatory fields: supplier and recipient GSTIN, HSN/SAC code, invoice number and date, description of goods or services, quantity, rate, tax amounts, and signatures.

- Confirm continuity in the invoice numbering system and proper issuance of credit/debit notes.

3. Input Tax Credit (ITC) Validation

- Verify eligibility of ITC claimed based on the nature of purchases and usage.

- Ensure ITC is not claimed on blocked credits under Section 17(5) of the CGST Act.

- Check reversals of ITC, if any, in accordance with rules 42 and 43.

- Ensure timely payment to vendors within 180 days to retain ITC eligibility.

4. Turnover and Exemptions Review

- Match declared turnover in returns with books of accounts and financial statements.

- Validate exemptions claimed with proper documentation and rule-based eligibility.

- Confirm correct GST rates are applied to taxable supplies.

5. Refund Claims Scrutiny

- Examine refund applications along with supporting documents.

- Ensure refunds are claimed under appropriate heads (inverted duty, export without payment, etc.).

- Check the justification and reconciliation of refund amounts claimed with returns and bank statements.

6. Record Maintenance

- Confirm maintenance of all required documents under Section 35 of the CGST Act.

- Ensure proper filing of contracts, purchase orders, payment proofs, e-way bills, and stock registers.

- Retain records for the statutory period of 6 years from the due date of the annual return for the relevant year.

VI. Key Points for Indian Businesses

GST audits are more than just compliance checks—they are instruments that safeguard the integrity of the indirect tax ecosystem. For Indian businesses, understanding the implications and expectations of a GST audit is critical.

1. GST Audit as a Compliance Tool

- The audit serves as a mechanism for the government to verify the accuracy of returns filed, taxes paid, and input tax credits claimed.

- It promotes transparency and accountability, both for businesses and the tax administration.

2. Importance of Proper Recordkeeping

- Maintaining accurate, updated, and complete records is non-negotiable. Businesses should have systems in place to ensure that all transactions—sales, purchases, credits, and refunds—are traceable and well-documented.

- Improper or incomplete documentation may invite penalties or adverse findings during the audit.

3. Timely Response to Audit Notices

- Ignoring or delaying a response to audit notices can escalate matters. Businesses are expected to cooperate fully and provide all relevant documents promptly.

- An audit notice typically provides at least 15 days’ time to prepare—use this window efficiently to organize data and seek professional support if needed.

4. Risk of Penalties for Non-compliance

- Discrepancies or willful misreporting discovered during the audit may lead to penalties, interest liabilities, or even prosecution under Section 73 (for non-fraud cases) or Section 74 (for fraud cases).

- Regular self-audits can help detect and rectify issues in advance, reducing the risk of such consequences.

5. Role of Professionals

- Chartered Accountants, Cost Accountants, and GST consultants play a crucial role in guiding businesses through audits. Their expertise in law, documentation, and reconciliation can be the difference between a smooth audit and a problematic one.

- Seeking professional advice proactively is a sound strategy, especially in complex or high-value cases.

Conclusion

A GST audit is not merely a statutory formality — it is a powerful instrument for both taxpayers and the government to ensure that the Goods and Services Tax regime functions with integrity, accuracy, and transparency. For Indian businesses, being audit-ready means maintaining clean records, reconciling returns consistently, and ensuring proper tax credit claims and filings.

By understanding the different types of audits, their triggers, processes, and potential consequences, businesses can better prepare for scrutiny and reduce risks of penalties or litigation. Proactive compliance, timely responses, and professional assistance when needed are essential to navigating a GST audit smoothly.

Frequently Asked Questions

1. Who is liable for a GST audit in India?

Under the current GST framework, the audit by a tax authority may be initiated for any registered taxpayer based on risk parameters, complexity of transactions, or discrepancies found during routine assessments. While the earlier threshold-based audit under Section 35(5) has been omitted, departmental and special audits under Sections 65 and 66 still apply.

2. What documents are required during a GST audit?

Documents generally required include GST returns (GSTR-1, GSTR-3B, GSTR-9), invoices, e-way bills, purchase and sales registers, input tax credit ledgers, reconciliation statements, financial statements, and refund applications.

3. What is the difference between a departmental audit and a special audit under GST?

A departmental audit (Section 65) is conducted by tax authorities and is part of routine compliance checks. A special audit (Section 66), however, is ordered by the Commissioner when complexity or discrepancies demand expert intervention, and is conducted by a CA or CMA nominated by the department.

4. How long does a GST audit take to complete?

A GST departmental audit must be completed within 3 months from the date of commencement. However, the Commissioner may extend this period by an additional 6 months in special circumstances. The final report is issued within 30 days of completion.

5. What happens if discrepancies are found during a GST audit?

If the audit reveals short payment of tax, excess refund, or ineligible input tax credit, the authorities may issue a Show Cause Notice under Section 73 or 74. The taxpayer may either contest the claim or make the necessary payment to settle the matter.