Filing your Income Tax Return (ITR) isn’t just about reporting numbers; it’s about making choices that directly affect your wallet. One of the most crucial decisions every taxpayer in India faces today is: Old Tax Regime or New Tax Regime: which one should you choose?

Even salaried individuals with a steady paycheck can legally save ₹20,000, ₹50,000, or even ₹1 lakh or more simply by selecting the regime that best fits their financial profile.

In this guide, we’ll simplify the complex and give you a crystal-clear understanding of how each regime works, so you can file your ITR confidently and maximize your savings.

Quick Snapshot: Old vs. New Tax Regime (FY 2025-26)

Before we dive deep, here’s a side-by-side snapshot to help you instantly grasp the core differences between the two regimes under current rules:

Feature | Old Tax Regime | New Tax Regime (FY 2025-26) |

Tax Rates | Higher rates, fewer slabs | Lower rates, more slabs |

Deductions & Exemptions | 70+ allowed (80C, HRA, LTA, etc.) | Most disallowed; very few permitted |

Standard Deduction | ₹50,000 (increased for the new regime) | ₹75,000 |

Rebate under Section 87A | ₹5 lakh income limit (₹12,500 rebate) | ₹12 lakh income limit (₹25,000 rebate) |

Default Option | No (must opt-in manually) | Yes (default from FY 2024-25) |

Switching Flexibility | Allowed yearly (non-business income) | Allowed yearly (non-business income) |

Ease of Filing | More paperwork, documentation-heavy | Simpler filing with fewer document |

Deep Dive: Understanding Both Tax Regimes

When it comes to Indian income tax, there’s no universal best-fit option. Your ideal regime depends on how you earn, save, and spend. Let’s break down each regime with crystal clarity.

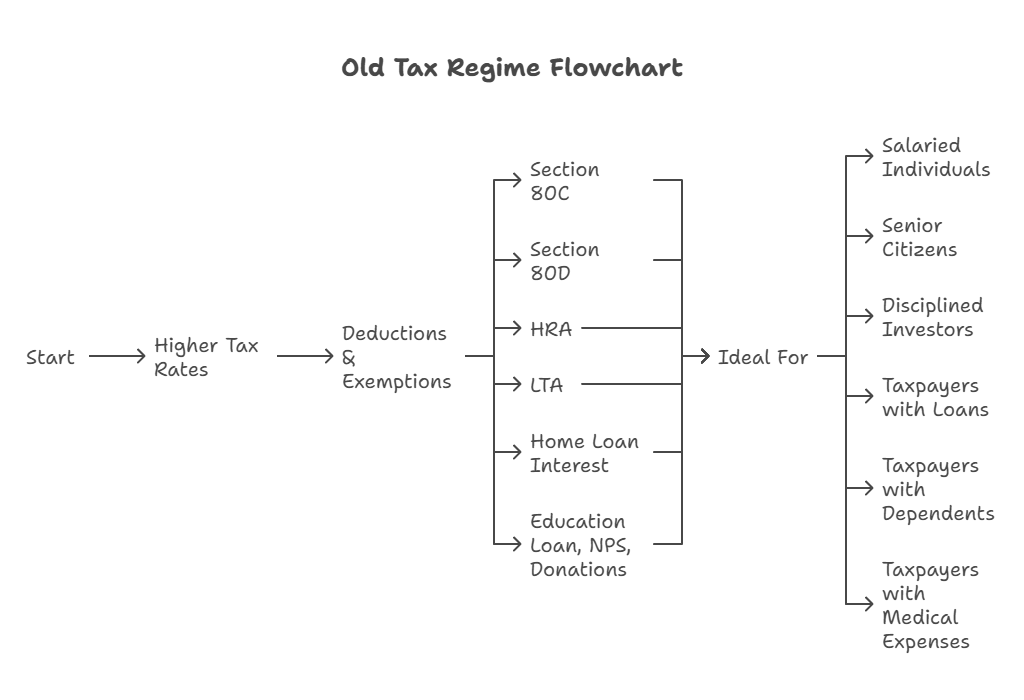

Old Tax Regime: The Traditional Route

The Old Tax Regime is like the “grandfather plan” of Indian taxation, built for those who love detailed tax planning and making the most of every deduction and exemption available.

Key Highlights:

✅ Higher Tax Rates, But Loaded With Deductions

The slabs here are steeper, but taxpayers can significantly reduce taxable income through deductions.

✅ 70+ Deductions & Exemptions Available:

- Section 80C: Up to ₹1.5 lakh (LIC, PPF, ELSS, NSC, etc.)

- Section 80D: Medical insurance premiums.

- HRA (House Rent Allowance): For salaried individuals living on rent.

- LTA (Leave Travel Allowance): Tax benefits on domestic travel.

- Home Loan Interest: Deduction on interest paid under Section 24(b).

- Education Loan, NPS, Donations, and more.

✅ Ideal For:

- Salaried individuals with high deductions.

- Senior citizens with interest income (Section 80TTB benefit).

- Disciplined investors maximize eligible deductions.

- Taxpayers with housing loans, dependents, or medical expenses.

📝 ReturnFile Pro Tip:

If your total deductions exceed ₹3 to ₹4 lakh, chances are high that the old regime will work better for you.

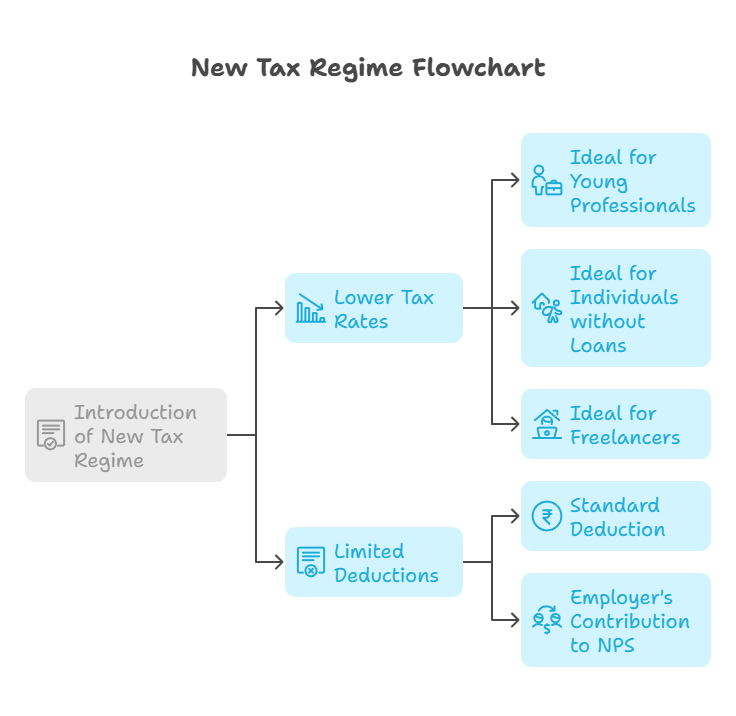

New Tax Regime: The Simplified Approach

Introduced to simplify taxation and reduce paperwork, the New Tax Regime strips away most deductions and offers lower, flatter tax slabs.

Key Highlights:

✅ Lower Tax Rates, More Slabs

Tax rates are lower across multiple income brackets, making it attractive for those without significant deductions.

✅ Limited Deductions Allowed:

- Standard Deduction: ₹75,000

- Employer’s Contribution to NPS: Still eligible.

- Most other deductions and exemptions are not permitted.

✅ Ideal For:

- Young professionals are starting their careers.

- Individuals without home loans, insurance investments, or rent expenses.

- Freelancers or consultants with straightforward income profiles.

- Taxpayers prefer ease, transparency, and minimal paperwork.

📝 ReturnFile Pro Tip:

If your gross income is up to ₹12.75 lakh (post-standard deduction), you may end up paying zero tax under the new regime.

Who Can Switch? Flexibility Rules

Understanding your ability to switch between regimes is just as important as knowing which regime suits you.

🔄 Eligibility Rules:

✅ Salaried Individuals (No Business Income):

You can switch between the Old and New Regime every financial year while filing your ITR.

✅ Individuals with Business or Professional Income:

- You can opt out of the new regime only once.

- Once you switch back to the Old Regime after opting out, you can’t revert to the New Regime again unless you discontinue your business/profession.

📅 Annual Review is Key

- Every year, assess your salary structure, deductions, new investments, and life changes (marriage, kids, loans).

- Consult with ReturnFile’s Experts to simulate both scenarios before filing.

📝 ReturnFile Pro Tip:

Don’t let default settings make decisions for you. Run the math each year, and your ideal tax regime can change as your income and investments evolve.

Which Regime is Right for You? — Decision Matrix

Choosing your tax regime isn’t about guesswork; it’s about matching your financial reality with what each regime offers. Here’s your decision cheat-sheet:

When the Old Tax Regime Makes Sense

✅ You Have High Deductions:

If you’re maxing out deductions like 80C (LIC, PPF, ELSS), 80D (medical insurance), HRA, LTA, home loan interest, and more, the old regime helps you convert these into big tax savings.

✅ You’re a Senior Citizen:

Higher exemption limits, plus additional benefits like Section 80TTB (interest income exemption up to ₹50,000), make the old regime attractive for retirees.

✅ Complex Income Sources With Exemptions:

If you have multiple income heads — salary, rental income, interest, capital gains, and can claim exemptions under multiple sections, the old regime offers flexibility to reduce taxable income.

✅ You’re Committed to Tax-Optimized Investing:

For disciplined savers who actively plan investments each year to maximize deductions, the old regime delivers better tax outcomes.

📝 ReturnFile Insight:

If your deductions regularly cross ₹3–4 lakh annually, the Old Regime will likely give you superior tax benefits.

When the New Tax Regime Makes Sense

✅ You Have Fewer Deductions:

If you’re not investing heavily in tax-saving instruments or your employer’s salary structure doesn’t offer HRA, LTA, or home loan benefits, New Regime’s flat rates often work better.

✅ You Prefer Simplicity:

No need to track dozens of documents or coordinate with your employer’s payroll for exemptions. Simple income, simple return.

✅ Income Up to ₹12.75 Lakh:

Under the new regime (post standard deduction), if your taxable income stays below ₹12.75 lakh, you may not pay any tax at all.

✅ You Want Minimal Paperwork:

No need for investment proofs, rent receipts, or medical bills, perfect for young professionals, freelancers, or anyone with limited tax planning bandwidth.

Practical Case Studies & Examples

Let’s bring theory to life with real-world examples:

🎯 Case 1: ₹13.75 lakh Salary — Old Regime Wins

- Income: ₹13,75,000

- Assumed Deductions (80C, 80D, HRA, LTA, etc.): ₹5,25,000

- Tax Calculation:

O Old Regime Tax Payable: ₹57,500

O New Regime Tax Payable: ₹75,000

✅ Verdict:

Old Regime delivers better savings here, thanks to significant deductions reducing taxable income.

🎯 Case 2: ₹20 lakh Salary — New Regime Wins

- Income: ₹20,00,000

- Assumed Deductions : Minimal or none (say, under ₹2 lakh)

- Tax Calculation:

O Old Regime Tax Payable: ₹2,40,000 (with ₹5.25 lakh deductions)

O New Regime Tax Payable: ₹2,00,000

✅ Verdict:

The New Regime is more tax-efficient here when deductions are low or negligible.

Summary Table: Quick Comparison Recap

Criteria | Old Tax Regime | New Tax Regime (FY 2025-26) |

Tax Slabs | Higher rates, fewer slabs | Lower rates, more slabs |

Deductions Allowed | 70+ deductions (80C, 80D, HRA, LTA, etc.) | Very limited (Standard Deduction ₹75,000) |

Rebate Limit (87A) | Up to ₹5 lakh income | Up to ₹12 lakh income |

Ease of Filing | Complex; documentation required | Simple, minimal paperwork |

Ideal For | High deductions, disciplined investors | Low deductions, simplicity seekers |

Default Option | No | Yes (from FY 2024-25) |

Switching Flexibility | Annual for salaried (if no business income) | Annual for salaried (if no business income) |

Senior Citizen Benefit | Section 80TTB, higher exemptions | Standard deduction applies, fewer benefits |

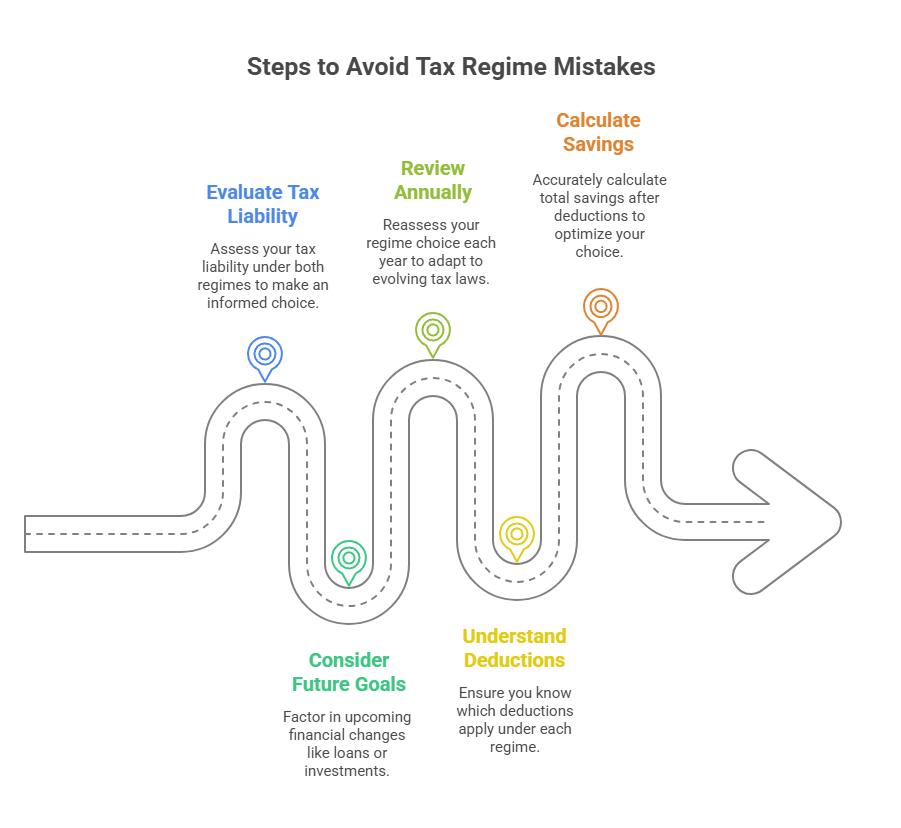

Common Mistakes Taxpayers Make While Choosing a Regime

Even after knowing the rules, many taxpayers fall into these traps, and they might make some mistakes while filing their ITR:

🚫 1. Blindly Selecting the Default Regime

Many simply go with the pre-selected regime while filing ITR, without evaluating their actual tax liability under both options.

🚫 2. Ignoring Future Financial Goals & Tax Planning

Choosing a regime based only on current income without factoring in upcoming loans, investments, or major life changes can cost you.

🚫 3. Not Reviewing the Regime Annually

Tax-saving options evolve; what worked last year may not work this year. Failing to reassess each financial year can lead to unnecessary tax outgo.

🚫 4. Misunderstanding Dedication Eligibility

Incorrect assumptions about which deductions apply under each regime often lead to miscalculation.

🚫 5. Overestimating or Underestimating Actual Savings

Many taxpayers don’t accurately calculate total savings after deductions, leading to a suboptimal regime choice.

Conclusion: Personalized Calculations Are Key

Choosing between the old and new tax regimes isn’t a one-size-fits-all decision. Your income, deductions, lifestyle, and financial goals play a huge role in determining which option saves you more.

💡 The smart move?

👉 Run calculations for both regimes before filing.

👉 Factor in upcoming investments, loans, and life changes.

👉 And if you’re unsure, let ReturnFile’s tax experts or our easy-to-use tax calculator do the heavy lifting for you.

✅ One correct decision today can save you thousands tomorrow.

Frequently Asked Questions

Q1. Can I change tax regimes every year?

Yes — salaried individuals without business income can switch regimes each financial year while filing ITR.

Q2. Is the new tax regime mandatory now?

The new tax regime is the default from FY 2024-25, but you can still opt for the old regime if eligible deductions make it beneficial.

Q3. Which deductions are allowed in the new regime?

Only a few, like the standard deduction (₹75,000), employer NPS contribution, and select allowances. Most other deductions (80C, HRA, etc.) are not allowed.

Q4. Are senior citizens better off in the old regime?

Generally, yes, because of additional exemptions like 80TTB and higher basic exemption limits in certain cases.

Q5. Is it true that income up to ₹12.75 lakh is tax-free under the new regime?

Effectively, yes — after standard deduction and rebate under section 87A, your tax liability could become zero if income stays within ₹12.75 lakh.

Q6. Do I need to submit proofs if I choose the new regime?

No, since most deductions are not allowed, documentation requirements are minimal under the new regime.

Q7. Which tax regime is better for freelancers or consultants?

It depends on their deductions and investments. Typically, if business-related deductions and expenses are significant, the old regime may offer better benefits.