Top 10 Mistakes to Avoid While Filing Income Tax Return in 2025.

I. Introduction

The Income Tax Department has significantly upgraded its monitoring capabilities in recent years. Integration of databases such as Form 26AS, Annual Information Statement (AIS), and Taxpayer Information Summary (TIS) means that any mismatch in reported income or deductions is quickly flagged for review. Additionally, the 2025 ITR forms introduce several new fields and validations, especially for capital gains, long-term asset disclosures, and deductions under the old regime.

II. Why Avoiding Mistakes Matters in 2025

The Income Tax Department has significantly upgraded its monitoring capabilities in recent years. Integration of databases such as Form 26AS, Annual Information Statement (AIS), and Taxpayer Information Summary (TIS) means that any mismatch in reported income or deductions is quickly flagged for review. Additionally, the 2025 ITR forms introduce several new fields and validations, especially for capital gains, long-term asset disclosures, and deductions under the old regime.

Here’s why it is critical to avoid errors in this year’s ITR:

- Increased scrutiny and automation: Returns are increasingly assessed through automated systems. Errors can trigger automatic notices or defective return flags.

- Higher financial penalties: Mistakes like under-reporting of income or claiming ineligible deductions can attract penalties of up to 200% of the tax due.

- Refund delays: Even small mismatches can hold up your refund for weeks or months while the return undergoes manual review.

- Invalid returns: Failing to e-verify the return or choosing an incorrect ITR form can render your return invalid, as if it were never filed.

By staying updated on the latest filing requirements and proactively avoiding common mistakes, taxpayers can ensure timely compliance and reduce the risk of future tax issues.

III. The Top 10 Mistakes You Must Avoid While Filing ITR in 2025

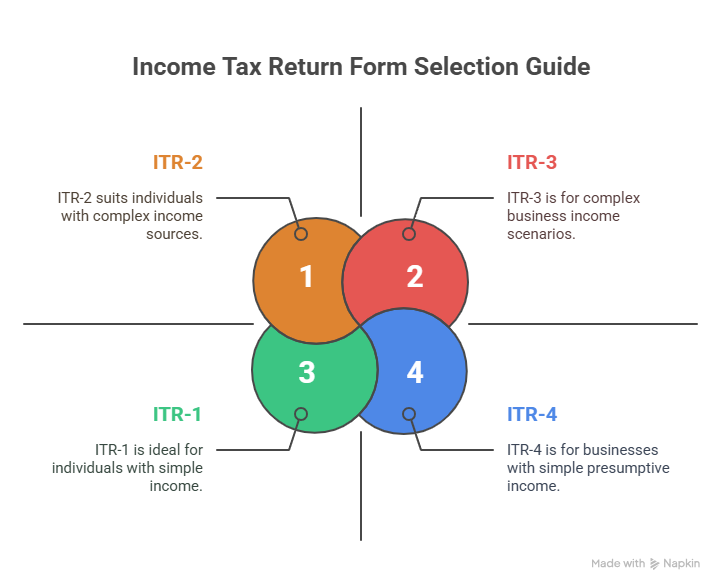

1. Selecting the Wrong ITR Form

One of the most common and costly mistakes taxpayers make is selecting an incorrect Income Tax Return (ITR) form. Each form is tailored to specific income profiles, and using the wrong one can result in your return being marked as “defective.” In such cases, you may receive a notice under Section 139(9), requiring you to file a corrected return within a specified period.

For Assessment Year 2025–26, the ITR forms have been updated to include new fields and disclosures. Here’s a brief snapshot:

- ITR-1 (Sahaj): Only for resident individuals with income up to ₹50 lakh from salary, one house property, and other sources like interest income. Not for those with capital gains, foreign income, or agricultural income exceeding ₹5,000.

- ITR-2: Suitable for individuals and HUFs not having income from business or profession but having income from capital gains, more than one house property, or foreign assets/income.

- ITR-3: For individuals and HUFs with income from business or profession.

- ITR-4 (Sugam): For presumptive taxation scheme users under Sections 44AD, 44ADA, or 44AE, with income up to ₹50 lakh.

Why it matters:

Using an incorrect form can lead to processing delays, defective return notices, or even rejection of your return.

How to avoid it:

Carefully review the instructions issued with each ITR form. If unsure, consult a tax professional or use the online utility on the Income Tax Department’s portal, which provides guided assistance in form selection.

2. Not Reconciling with Form 26AS, AIS, and TIS

Before filing your return, it’s essential to reconcile the income and tax details with Form 26AS, the Annual Information Statement (AIS), and the Taxpayer Information Summary (TIS). These documents capture the data reported by employers, banks, mutual funds, registrars, and other third parties to the Income Tax Department.

Common mismatches include:

- Interest income from fixed deposits not matching AIS entries

- Dividend income missed from TIS.

- TDS claimed in return but not reflected in Form 26AS

- The purchase/sale of mutual funds or stocks was not disclosed properly.

Why it matters:

Discrepancies between your ITR and these statements can trigger scrutiny or delay refunds. In some cases, it may even lead to a tax demand if under-reporting is established.

How to avoid it:

- Download Form 26AS and AIS from the Income Tax e-filing portal

- Cross-check each item with your bank statements, salary slips, Form 16, and investment report.s

- Report and correct any mismatches before filing your return

3. Missing the New Documentation Requirements (Old Regime)

If you are opting for the old tax regime in AY 2025-26, simply relying on Form 16 is no longer sufficient. The Central Board of Direct Taxes (CBDT) has introduced stricter documentation protocols. This means that to claim deductions under various sections, such as 80C, 80D, 80G, and HRA, you must now be able to substantiate each claim with proper proof.

Key documentation includes:

- Section 80C: PPF deposit slips, LIC premium receipts, ELSS investment statements

- Section 80D: Health insurance premium paid receipts for self and family

- House Rent Allowance (HRA): Rent receipts, rent agreement, landlord’s PAN (if rent exceeds ₹1 lakh annually)

- Section 80G: Donation receipts with 80G certificate details

Why it matters:

Incomplete or missing documentation may lead to the disallowance of deductions, increasing your tax liability. During processing or in case of scrutiny, you may be asked to submit proof of all deductions claimed.

How to avoid it:

- Maintain a valid rent agreement and periodic rent receipts with payment proof.

- Obtain the landlord’s PAN where applicable.

- Ensure the claimed address matches your employment records and utility bills, substantiating actual residence.

4. Overlooking Income from Previous Employers

If you changed jobs during FY 2024–25, it’s vital to declare salary income from all employers in your ITR. A common mistake is to file using only the latest employer’s Form 16, which often leads to incorrect computation of total income and tax due.

Here’s what happens if you omit a previous employer:

- You may end up double-claiming the basic exemption limit and standard deductions.

- Deductions under 80C, HRA, or 80D might be applied twice across two employers, flagging your return for tax mismatch.

- The total tax deducted by each employer may be insufficient, leading to a tax demand and interest under Section 234B/234C.

Why it matters:

Failure to report salary from previous employment can trigger notices, tax demands, and penalties for under-reporting income.

How to avoid it:

- Request Form 16 from all past employers and compile them before filing.

- Use the consolidated salary income to compute your tax.

- Review Form 26AS and AIS to cross-check the total TDS and income details.

5. Not Reporting All Income Sources

Many taxpayers focus only on their primary salary or business income and inadvertently ignore smaller or secondary income streams. However, the Income Tax Department now receives extensive third-party data, making non-reporting easily detectable through AIS and TIS.

Commonly missed income includes:

- Savings account interest

- Fixed deposit (FD) interest

- Recurring deposit (RD) interest

- Dividend income from shares or mutual funds

- Rental income from property

- Capital gains from the sale of shares, mutual funds, or property

- Foreign income or assets (for resident taxpayers)

Remember, even tax-exempt income (like certain agricultural income or PPF interest) may still need to be disclosed in the ITR for transparency.

Why it matters:

Under-reporting of income can attract severe consequences, including tax demands, interest, penalties under Section 270A (which allows penalties up to 200%), and possible scrutiny notices.

How to avoid it:

- Review your bank statements, Demat accounts, Form 26AS, AIS, and TIS carefully.

- Report all income, whether taxable or exempt.

- Claim available deductions (such as Section 80TTA or 80TTB for savings interest) after reporting the full income.

6. Errors in HRA Declarations

House Rent Allowance (HRA) remains one of the most scrutinized deductions, especially in cases where taxpayers claim inflated or unsupported HRA deductions.

Common mistakes include:

- Not maintaining rent receipts or rent agreements

- Failing to provide the landlord’s PAN where the annual rent exceeds ₹1 lakh

- Claiming HRA without actually residing in the rented property

- Not maintaining rent receipts or rent agreements

Why it matters:

If discrepancies are found during processing or scrutiny, the tax authorities may disallow the HRA exemption and levy penalties up to 200% of the incorrect claim.

How to avoid it:

- Maintain a valid rent agreement and periodic rent receipts with payment proof.

- Obtain the landlord’s PAN where applicable.

- Ensure the claimed address matches your employment records and utility bills, substantiating actual residence.

7. Missing the Filing Deadline

Filing your Income Tax Return after the due date is one of the most avoidable mistakes, yet every year, thousands of taxpayers miss the deadline due to poor planning or last-minute delays.

For Assessment Year 2025–26, the deadline has been extended to September 15, 2025 for most individual taxpayers (non-audit cases).

Consequences of missing the deadline include:

- Late filing fees under Section 234F (up to ₹5,000)

- Interest liability under Sections 234A, 234B, and 234C for any outstanding tax

- Loss of certain deductions or exemptions that are only allowed in returns filed on time

- Inability to carry forward certain capital losses or business losses

Why it matters:

Late filing not only attracts penalties but may also delay your refund processing or increase future tax liabilities.

How to avoid it:

- Begin tax preparation early, ideally as soon as Form 16, Form 26AS, AIS, and TIS are available.

- Use professional help or reliable tax filing platforms if needed.

- Avoid waiting until August or September when portal traffic is heavy and processing times are slower.

8. Not Claiming All Eligible Deductions and Exemptions

Even after paying taxes, many taxpayers unknowingly leave money on the table by failing to claim all deductions they’re entitled to, especially under the old tax regime.

Commonly overlooked deductions include:

- Section 80C: Life insurance premiums, PPF, ELSS, children’s tuition fees, principal repayment on home loan

- Section 80D: Health insurance premiums for self, family, and parents

- Section 80E: Interest on education loans

- Section 24(b): Home loan interest on self-occupied or let-out property

- Section 80G: Donations to eligible charities

- Section 80TTA/80TTB: Interest on savings accounts for general taxpayers and senior citizens

- Standard deduction for pensioners and salaried individuals

Why it matters:

Overlooking eligible deductions results in higher tax outgo than necessary and could impact your overall financial planning.

How to avoid it:

- Prepare a comprehensive deduction checklist before filing.

- Keep all supporting documents and receipts ready and organized.

- Regularly consult with your tax advisor to ensure you are availing of all possible benefits.

9. Not E-Verifying the ITR

Many taxpayers believe that once they have submitted their Income Tax Return online, their filing is complete. However, e-verification is a mandatory step to complete the filing process. If your ITR is not verified within the prescribed timeline, it will be treated as invalid.

For AY 2025–26, the Income Tax Department requires e-verification to be completed within 30 days of filing.

Methods of e-verification include:

- Aadhaar-based OTP

- Net banking authentication

- Demat account verification

- Bank account-based EVC (Electronic Verification Code)

Why it matters:

Failure to e-verify results in the return being treated as non-filed, exposing the taxpayer to penalties, interest, and loss of deductions or refunds.

How to avoid it:

- Immediately verify your return after submission.

- Use Aadhaar OTP or net banking for quicker verification.

- Check the ITR portal dashboard to ensure verification status reflects as “Successfully Verified.

- Immediately verify your return after submission.

10. Ignoring New Reporting Requirements and Form Changes

For AY 2025–26, several changes have been introduced in the ITR forms that taxpayers must carefully review before filing.

Key updates include:

Revised reporting for capital gains with a detailed breakup across asset categories.

- Reporting of Long-Term Capital Gains (LTCG) at updated tax rates.

- Disclosure of Aadhaar enrolment ID where PAN is not yet linked or allotted.

- Expanded sections in AIS and TIS capture diverse income streams and high-value transactions.

Why it matters:

Failure to comply with the latest reporting requirements may result in your return being flagged as defective or incomplete, inviting scrutiny, delays, or penalties.

How to avoid it:

- Read the official ITR form instructions issued by the Income Tax Department.

- Stay updated through reliable financial news sources or consult your tax advisor.

- Use updated tax software or online portals that reflect the latest changes for AY 2025–26.

Conclusion: Filing Right, Filing Smart

Income Tax Return filing for AY 2025–26 comes with both opportunities and pitfalls. With stricter reporting standards, expanded disclosures, and data-driven scrutiny by the Income Tax Department, even minor errors can lead to serious complications.

By carefully avoiding these 10 common mistakes, staying updated with the latest filing rules, and preparing documentation in advance, taxpayers can ensure:

- Accurate filings

- Timely refunds

- Reduced chances of scrutiny or penalties

For those uncertain or overwhelmed, seeking professional assistance from trusted tax consultants or platforms can simplify the process and bring peace of mind.

Frequently Asked Questions?

Q1. What are the most common mistakes while filing ITR in 2025?

The most common mistakes include selecting the wrong ITR form, not reconciling Form 26AS/AIS/TIS, missing documentation under the old regime, failing to report income from previous employers, and not e-verifying the return on time.

Q2. What happens if I select the wrong ITR form?

Q2. What happens if I select the wrong ITR form?

If you choose an incorrect ITR form, your return may be marked defective by the Income Tax Department, leading to notices, delayed processing, or rejection.

Q3. Do I need to report all income even if tax is not deducted?

Yes. All income, including savings account interest, fixed deposit interest, rental income, and dividends, must be reported, even if tax was not deducted at source.

Q4. What documents are required for ITR filing under the old tax regime?

You need supporting documents for deductions claimed, such as Form 16, rent receipts, insurance premiums, investment proofs (PPF, ELSS, LIC), medical insurance, and donation receipts.

Q5. What is the deadline for filing ITR for AY 2025-26?

For Assessment Year 2025-26, the extended deadline to file ITR is September 15, 2025.