GST E-Way Bill Services in India: A Comprehensive Guide

I. Introduction

The Goods and Services Tax (GST) regime in India, introduced in July 2017, was a landmark reform aimed at creating a unified tax structure across the country. By subsuming multiple indirect taxes and introducing a destination-based taxation system, GST simplified compliance, increased transparency, and enhanced the ease of doing business.

One of the critical pillars supporting this regime is the E-Way Bill system. Introduced to streamline the movement of goods and prevent tax evasion, the E-Way Bill is a digital document generated for tracking consignments in transit. It plays a key role in digitizing logistics and ensuring real-time compliance under the GST framework.

The E-Way Bill system brings standardization, efficiency, and visibility into the movement of goods across state and intra-state boundaries. For businesses, it has reduced transit delays and administrative hurdles. For tax authorities, it serves as a robust tool for monitoring transactions and curbing evasion.

II. What is an E-Way Bill?

An E-Way Bill (Electronic Way Bill) is a mandatory document required for the transportation of goods valued above ₹50,000. It is generated electronically through the GST E-Way Bill portal before the commencement of movement of goods. Whether the transaction is a sale, return, or inward supply from an unregistered dealer, an E-Way Bill must be generated if the value exceeds the specified threshold.

The concept was introduced under Rule 138 of the CGST Rules, empowering tax authorities to track the movement of goods and ensure tax accountability. The system integrates various stakeholders—suppliers, recipients, transporters—and provides a seamless digital interface for compliance.

Who Needs to Generate an E-Way Bill?

The responsibility to generate an E-Way Bill depends on the nature of the transaction and the parties involved:

- Registered suppliers transporting goods worth more than ₹50,000.

- Registered recipients, in cases where the supplier is unregistered.

- Transporters, when neither the supplier nor the recipient generates the bill.

- Unregistered persons, in specific cases of inward supply.

It is mandatory for inter-state movement and, in many states, for intra-state movement as well. Exemptions apply to specific categories of goods, including perishable items and those listed in government notifications.

III. Applicability and Threshold

The E-Way Bill system has clearly defined applicability criteria based on the value of goods and the nature of movement.

1. Value Threshold: ₹50,000 and Above

An E-Way Bill is mandatory when the consignment value exceeds ₹50,000, whether for a single invoice or multiple invoices in a single consignment. The value includes the taxable amount and applicable GST, but excludes the value of exempt goods in a mixed supply.

2. Inter-State vs Intra-State Movement

- Inter-State: The generation of an E-Way Bill is mandatory for all interstate transportation of goods, regardless of the distance.

- Intra-State: Each state has notified its own rules. In many states, E-Way Bills are required for intra-state movement above ₹50,000, though some provide higher thresholds or exemptions for certain goods.

3. Who is Responsible?

- Registered Person: The supplier or recipient, if registered, must generate the E-Way Bill.

- Transporter: If neither the supplier nor the recipient generates the bill, the responsibility shifts to the transporter.

- Unregistered Person: In certain cases (e.g., inward supply to a registered person), the recipient must generate the bill.

4. Exemptions and Special Cases

E-Way Bill is not required in the following situations:

- Transport of exempt goods (e.g., fresh fruits, vegetables, milk).

- Movement of goods under customs supervision or bond.

- Transport by non-motorized conveyance (e.g., hand carts).

- Transport of goods within a notified area (e.g., a municipality or urban limits) is exempted by the state.

Transit cargo to and from Nepal or Bhutan.

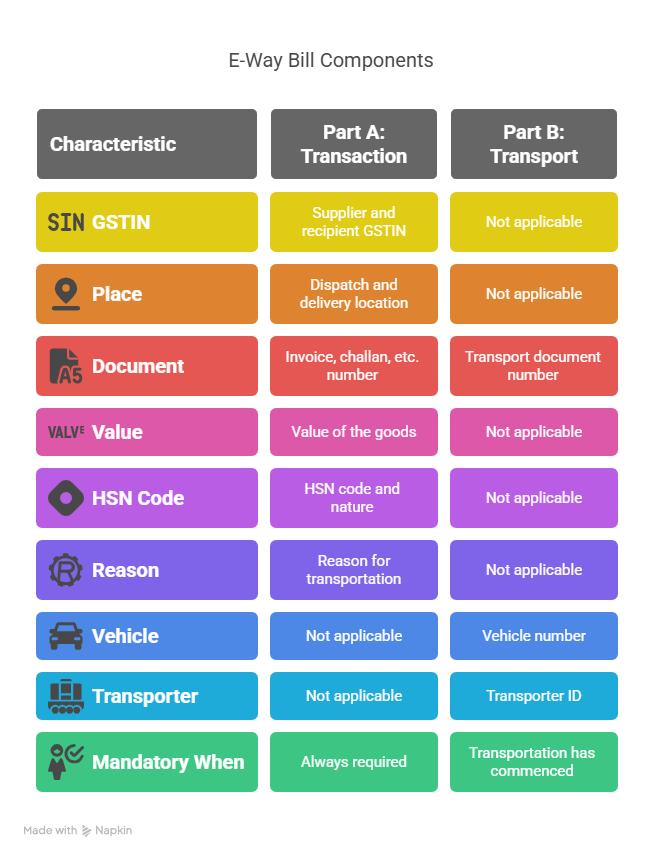

IV. Components of the E-Way Bill

The E-Way Bill is divided into two main parts, each capturing essential details for the transport and tracking of goods.

1. Part A: Transaction Details

Part A includes key transactional data:

- GSTIN of the supplier and recipient

- Place of dispatch and delivery

- Document number (invoice, bill of supply, delivery challan)

- Value of goods

- HSN code and nature of goods

- Reason for transportation (e.g., supply, return, job work)

This section is essential for identifying the parties and the goods involved in the movement.

2. Part B: Transport Details

Part B captures:

- Vehicle number for road transport

- Transport document number (GR/RR/Airway Bill number)

- Transporter ID (if movement is by a third-party logistics provider)

3. When is Part B Mandatory?

Part B is mandatory only when the transportation of goods has commenced. It is particularly essential in the following scenarios:

- Road transport via motor vehicle

- Movement by rail, air, or ship (Transporter ID and document number required)

Note: If the goods are moved in multiple stages or via transshipment, Part B must be updated at each stage with the correct vehicle details.

V. How to Generate an E-Way Bill

Generating an E-Way Bill is a mandatory step before the commencement of the movement of goods. The government has provided multiple channels to simplify the process for businesses of all sizes.

1. Methods of Generation

There are several ways to generate an E-Way Bill, depending on the business’s volume, scale, and technical infrastructure:

- Online Portal:

The most widely used method is the official E-Way Bill portal ewaybillgst.gov.in, where users can generate, update, and manage bills. - SMS-Based Generation:

Suitable for small businesses or transporters with limited internet access. Bills can be generated or cancelled via SMS using registered mobile numbers. - Mobile App:

The government provides a mobile app integrated with the portal, allowing users to generate E-Way Bills on the go. - API Integration:

Large organizations with ERP systems can integrate their software directly with the E-Way Bill system through APIs for seamless generation and data exchange. - Bulk Generation Tool:

For businesses generating multiple bills daily, the bulk upload facility enables faster processing by uploading data in a specified format.

2. Step-by-Step Process on the Online Portal

Here’s a simple walkthrough for generating an E-Way Bill via the portal:

- Login:

Visit ewaybillgst.gov.in and log in with your GST credentials. - Select “Generate New”:

From the dashboard, click on the “E-Way Bill” option and then “Generate New.” - Enter Transaction Details:

Fill in the required details in Part A:- Type of transaction (inward or outward)

- GSTIN of the supplier and recipient

- Document type and number (invoice, delivery challan)

- Product details, including HSN code, quantity, value, and tax rate

- Type of transaction (inward or outward)

- Enter Transport Details (Part B):

- Mode of transport (road, rail, air, or ship)

- Vehicle number or transporter ID

- Estimated distance

- Mode of transport (road, rail, air, or ship)

- Submit and Generate:

Once all fields are completed, click “Submit.” A unique E-Way Bill Number (EBN) will be generated. - Download/Print:

Print or download the E-Way Bill to ensure it accompanies the goods during transit.

VI. Recent Updates and Compliance Requirements

Staying updated with the latest amendments in E-Way Bill rules is crucial for businesses to remain compliant and avoid penalties. The GST Council and the CBIC frequently update rules to strengthen transparency, reduce tax evasion, and promote digitalization.

1. E-Invoicing Linkage (Effective March 1, 2024)

For taxpayers enabled for e-invoicing, it has become mandatory to auto-populate invoice-related data while generating E-Way Bills for:

- B2B transactions

- Exports

This integration eliminates manual errors, improves data accuracy, and reduces duplication of efforts between invoice and E-Way Bill generation.

2. Validity and Extension of E-Way Bill

- The validity period of an E-Way Bill is determined by the distance to be covered:

- Up to 100 km: 1 day

- Every additional 100 km or part thereof: 1 extra day

- Up to 100 km: 1 day

- Extension is allowed before expiry if there is a delay due to exceptional circumstances like natural calamities, law & order situations, etc.

The maximum permissible extension period is now capped at 360 days from the date of generation.

3. Blocking of E-Way Bill Generation

E-Way Bill generation may be blocked for taxpayers who:

- Have not filed GSTR-3B for two consecutive tax periods.

- Have been flagged by the GST department under the risk-based parameters.

This step enforces return filing discipline and filters out non-compliant businesses from the supply chain.

4. Penalties for Non-Compliance

Transporting goods without a valid E-Way Bill can result in:

- Penalty: ₹10,000 or the amount of tax sought to be evaded (whichever is higher).

- Detention or seizure of goods and vehicles.

- Additional interest or late fees if tax evasion is determined after audit or inspection.

Proper documentation during transport is essential to avoid unnecessary delays and legal consequences.

VII. Enforcement and Penalties

The E-Way Bill system is not merely a formality—it’s a legally enforceable component of the GST compliance ecosystem. Authorities across India are empowered to inspect, intercept, and act upon any discrepancies related to the movement of goods without a valid E-Way Bill.

1. Authority to Inspect and Verify

- GST officers and other empowered enforcement officials are authorized to intercept vehicles and verify E-Way Bills.

- Verification may be conducted physically or via RFID systems at check-posts or on highways.

- Officers can demand physical documents or e-documents on mobile devices for on-the-spot checks.

2. Consequences of Non-Compliance

Failure to produce a valid E-Way Bill during transport can result in the following enforcement actions:

- Detention or Seizure of Goods and Conveyance: Under Section 129 of the CGST Act, 2017, goods without valid documentation can be detained, and the vehicle may also be seized.

- Levy of Penalty:

- A minimum penalty of ₹10,000 or the amount of tax sought to be evaded, whichever is higher.

- In case of voluntary payment, goods may be released after the penalty is paid. Otherwise, adjudication proceedings may follow.

- A minimum penalty of ₹10,000 or the amount of tax sought to be evaded, whichever is higher.

3. Reporting Requirements for Officers

- After verification, the officer must submit a summary report online within three working days.

- If required, a final report must be uploaded within fifteen days.

- These timelines ensure transparency and accountability in enforcement activities.

4. Exceptions to Multiple Verifications

Once a vehicle has been inspected in one state and a report is filed, it cannot be inspected again in another state, unless there’s specific information indicating tax evasion.

5. Compliance for Businesses

Businesses should:

- Ensure proper training for logistics and transport teams.

- Maintain all documents in digital and physical formats during movement.

- Be prompt in responding to any notices or queries related to E-Way Bills.

- Ensure proper training for logistics and transport teams.

By following these practices, businesses can avoid penalties, delays, and disruptions in supply chains.

VIII. Benefits of the E-Way Bill System

The E-Way Bill system was introduced not just as a compliance requirement but also as a tool to improve efficiency, transparency, and integrity in the movement of goods across India. Here are some of the major benefits:

1. Seamless Movement of Goods

- Removal of physical check-posts has significantly reduced transit time and bottlenecks.

- Businesses can now move goods across states with minimal interruption, resulting in faster deliveries and improved service levels.

2. Enhanced Transparency and Tracking

- Every consignment is documented digitally, making it easier for authorities and businesses to track movement in real time.

- Reduces the scope for under-invoicing, duplicate billing, or misreporting of goods in transit.

3. Reduction in Tax Evasion

4. Exceptions to Multiple Verifications

- For businesses under the e-invoicing mandate, the E-Way Bill can be auto-populated from invoice data.

- This reduces manual errors and simplifies record-keeping and compliance.

5. Digital Efficiency

- Offers multiple modes of generation: Web, SMS, Mobile App, API, and Bulk Upload.

- Minimizes paperwork and allows businesses to maintain digital records that are easy to retrieve and audit.

6. Cost Savings for Businesses

- Reduces delays and fuel costs associated with stops and inspections.

- Enables better route planning and logistics optimization, especially for large transport operations.

7. Encourages a Uniform Tax Structure

- Facilitates consistent compliance practices across India.

- Promotes the government’s goal of a “One Nation, One Tax, One Market” framework under GST.

Frequently Asked Questions

1. Who is required to generate an E-Way Bill under GST?

Any registered person transporting goods worth more than ₹50,000—either interstate or intrastate—is required to generate an E-Way Bill. In some cases, even unregistered persons and transporters must generate it if they are involved in the movement of taxable goods.

2. Is an E-Way Bill required for the movement of exempted goods?

No, the E-Way Bill is not required for transporting goods that are wholly exempt from GST. However, if a consignment contains both exempt and taxable goods, the requirement may apply based on the total value and nature of the goods.

3. What happens if goods are moved without generating an E-Way Bill?

If goods are transported without a valid E-Way Bill where required, authorities can detain or seize the goods and vehicle. A penalty of ₹10,000 or the tax amount evaded (whichever is higher) may also be levied.

4. Can the validity of an E-Way Bill be extended?

Yes, the validity of an E-Way Bill can be extended before expiry under certain conditions, such as natural calamity, law and order issues, or vehicle breakdown. The extension must be done online through the portal.

5. Is Part B of the E-Way Bill always mandatory?

Part B, which contains the vehicle number or transporter ID, is mandatory when goods are being moved by road. However, for certain modes of transport like rail or air, Part B can be updated later under prescribed rules.