![How to File ITR for Senior Citizens in India [With Tax Benefits]](https://returnfile.in/wp-content/uploads/2025/06/How-to-File-ITR-for-Senior-Citizens-in-India-With-Tax-Benefits-1024x576.jpg)

Why Filing ITR is Crucial for Senior Citizens

For many senior citizens in India, income tax filing may feel like an unnecessary chore after decades of work. But here’s the truth: filing your Income Tax Return (ITR) is not just a legal formality; it’s a smart financial move that unlocks a host of tax benefits tailored specifically for you.

First, compliance keeps you on the right side of the Income Tax Department. Timely filing ensures your financial records remain transparent, making processes like loan applications, visa procedures, and wealth transfers far smoother. More importantly, filing allows you to claim your rightful deductions, avoid unnecessary tax deductions at source (TDS), and even secure refunds on any excess tax paid.

The government recognizes the unique financial circumstances of senior citizens, limited active income, reliance on pensions, and growing healthcare costs. That’s why, under India’s Income Tax Act, special exemptions, deductions, and simplified processes have been introduced exclusively for this age group.

And the good news? FY 2025-26 (AY 2026-27) brings some meaningful updates, higher exemption limits, increased TDS thresholds, and tax-free NSS withdrawals, among others. With these in place, filing ITR is not just easier, it’s financially rewarding.

Who Qualifies as a Senior Citizen & Super Senior Citizen?

Definition under the Income Tax Act

The Income Tax Act of India offers a clear, age-based classification when it comes to senior citizens:

- Senior Citizen: Any resident individual aged 60 years or above but below 80 years during the financial year.

- Super Senior Citizen: Any resident individual aged 80 years or above during the financial year.

This classification isn’t just for semantics; it directly influences your tax liabilities and the benefits you can claim.

Age-wise Categorization

Category | Age Group |

Senior Citizen | 60 years to <80 years |

Super Senior Citizen | 80 years and above |

Simply put: the day you turn 60, you step into the senior citizen bracket; cross 80, and you enjoy even higher tax relaxations as a super senior.

Impact of Classification on Tax Benefits

The age-based classification unlocks several perks:

- Higher Basic Exemption Limits: Senior citizens enjoy a basic tax exemption up to ₹3,00,000, while super seniors get an even bigger exemption of ₹5,00,000 under the old regime.

- Reduced Tax Burden: Lower taxable income means a smaller tax outgo, especially when combined with deductions like the standard deduction, 80TTB, and others.

- Simplified Compliance: Super senior citizens (80+) can even choose to file their returns offline, a rare privilege in today’s digital-first compliance system.

- Advance Tax Relaxation: If you don’t have business income, you’re not required to pay advance tax, allowing you to settle your taxes in one go at the time of filing.

In short, your age not only brings wisdom but also tax relief, provided you file your ITR timely and correctly.

Income Tax Slabs for Senior & Super Senior Citizens (FY 2025-26)

When it comes to income tax, age works in your favour. The government offers senior and super senior citizens a softer tax regime, making sure your golden years are financially comfortable. Let’s decode the slabs for FY 2025-26 (AY 2026-27).

Old Regime vs New Regime: What’s the Difference?

Category | Old Regime: Basic Exemption | New Regime: Basic Exemption |

Senior Citizen (60-79) | ₹3,00,000 | ₹4,00,000 |

Super Senior Citizen (80+) | ₹5,00,000 | ₹4,00,000 |

While both regimes offer tax relief, the Old Regime often remains popular among senior citizens due to additional deductions and exemptions. The New Regime, introduced to simplify taxation, offers lower tax rates but fewer deductions.

Detailed Slab Comparison

Old Tax Regime (Senior Citizens: 60–79 years)

Income Slab | Tax Rate |

₹0 – ₹3,00,000 | Nil |

₹3,00,001 – ₹5,00,000 | 5% |

₹5,00,001 – ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

Old Tax Regime (Super Senior Citizens: 80+ years)

Income Slab | Tax Rate |

₹0 – ₹5,00,000 | Nil |

₹5,00,001 – ₹10,00,000 | 20% |

Above ₹10,00,000 | 30% |

New Tax Regime (All Individuals, including Senior & Super Senior Citizens)

Income Slab | Tax Rate |

₹0 – ₹4,00,000 | Nil |

₹4,00,001 – ₹8,00,000 | 5% |

₹8,00,001 – ₹12,00,000 | 10% |

₹12,00,001 – ₹16,00,000 | 15% |

₹16,00,001 – ₹20,00,000 | 20% |

₹20,00,001 – ₹24,00,000 | 25% |

Above ₹24,00,000 | 30% |

Examples to Illustrate Tax Differences

Example 1: A 70-year-old senior citizen earning ₹6 lakh annually (Old Regime)

- Income: ₹6,00,000

- Basic Exemption: ₹3,00,000

- Taxable Income: ₹3,00,000

- Tax: ₹3,00,000 × 5% = ₹15,000

- Standard Deduction: ₹50,000 (brings taxable income down)

Example 2: An 82-year-old super senior citizen earning ₹7 lakh annually (Old Regime)

- Income: ₹7,00,000Basic Exemption: ₹5,00,000

- Taxable Income: ₹2,00,000

- Tax: ₹2,00,000 × 20% = ₹40,000

- After deductions and rebates = Effective tax is almost Nil or very low

The takeaway: Age plus the right deductions can shrink your tax bill dramatically.

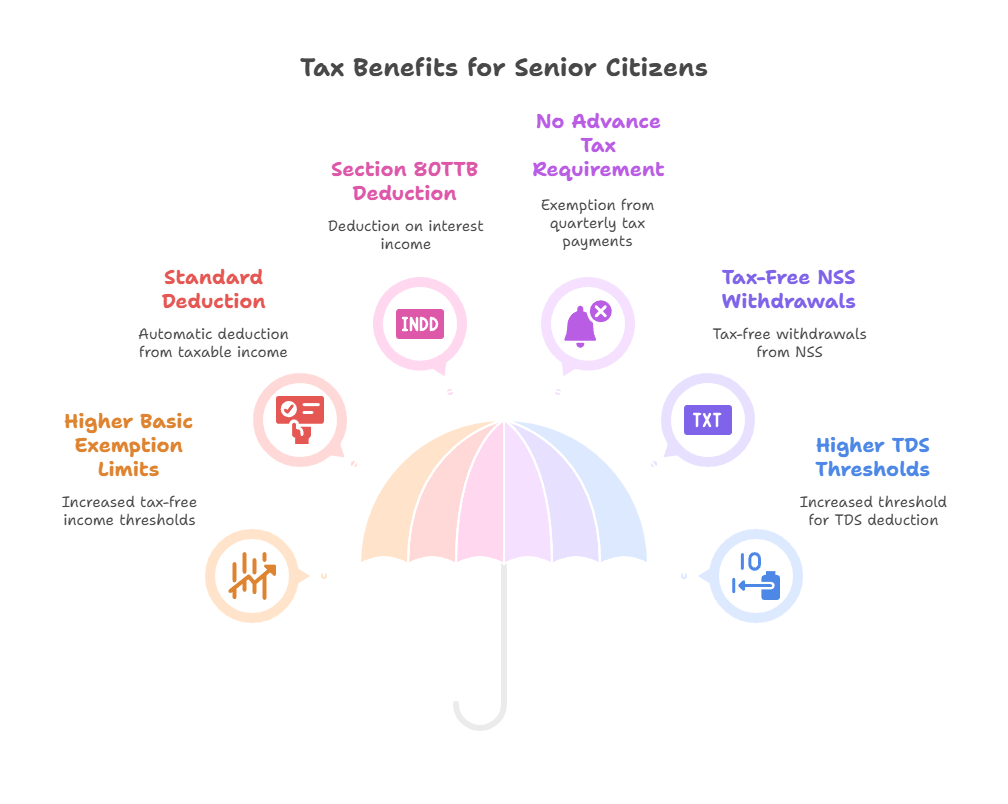

Special Tax Benefits Available for Senior Citizens

Now, for the real perks, let’s unlock the treasure chest of tax benefits that senior citizens enjoy under Indian tax laws.

1️⃣ Higher Basic Exemption Limits

- Senior Citizens: ₹3,00,000 (Old Regime)

- Super Senior Citizens: ₹5,00,000 (Old Regime)

- New Regime: ₹4,00,000 (flat for all)

2️⃣ Standard Deduction of ₹50,000

If you’re receiving pension or salary income, you automatically get a ₹50,000 deduction. Think of it as the government trimming ₹50,000 from your taxable income before applying tax rates. No paperwork. No questions asked.

3️⃣ Section 80TTB – Deduction on Interest Income

Senior citizens can deduct up to ₹50,000 from:

- Savings account interest

- Fixed deposits

- Recurring deposits

- Post office deposits

This is over and above the standard deduction and helps reduce tax on interest-heavy income streams.

4️⃣ No Advance Tax Requirement

Senior citizens without business income are spared from paying advance tax quarterly. Instead, you can pay your entire tax liability in one go while filing your return.

This makes cash flow management much easier, with no reminders, no penalties.

5️⃣ Tax-Free NSS Withdrawals

Effective August 29, 2024, withdrawals from the National Savings Scheme (NSS) are now completely tax-free for senior citizens.

This provides an additional liquidity cushion and one less item to worry about during tax filing.

6️⃣ Higher TDS Thresholds on Interest Income

From FY 2025-26, banks won’t deduct TDS on interest if:

- Your total interest income is below ₹1,00,000 annually (up from ₹50,000 earlier).

- This puts more cash in your hands throughout the year and minimizes refund hassles.

Section 4: Exemption from ITR Filing under Section 194P

While most taxpayers must file an ITR every year, certain senior citizens enjoy full exemption, thanks to Section 194P. Introduced to simplify life for India’s oldest taxpayers, this section relieves eligible individuals from the annual tax filing grind.

Eligibility Criteria: Are You Covered?

To qualify for exemption under Section 194P, you must tick all of these boxes:

✅ You are 75 years or older at any point during the financial year.

✅ You are a resident Indian.

✅ Your only sources of income are:

- Pension income

- Interest income (but only from the same specified bank where your pension is credited)

✅ You have submitted a valid declaration (Form 12BBA) to your bank.

⚠ Important: If you have additional income (like rent, capital gains, multiple bank accounts, business income, etc.), you do not qualify under Section 194P and must file your ITR as usual.

The Role of Form 12BBA

Form 12BBA is your official self-declaration to the bank, stating:

- Your income sources (only pension + interest)

- Details of deductions eligible under Chapter VI-A (like 80C, 80D, etc.)

- Your applicable tax regime (Old vs New)

- Confirmation that no other income sources exist

💡 Think of Form 12BBA as your personal ITR, but handled entirely by your bank.

Responsibilities of Specified Banks

Once you submit Form 12BBA, the bank takes over:

✅ Computes your total income

✅ Applies all applicable deductions

✅ Calculates your tax liability

✅ Deducts TDS accordingly

✅ Submits details to the Income Tax Department

You don’t need to lift a finger beyond this point, provided your bank gets it right.

Limitations: When You Still Need to File ITR

You are still required to file ITR if:

- You have income beyond pension + specified interest.

- You have multiple bank accounts.

- You receive rental income, capital gains, foreign income, or business income.

- You failed to submit Form 12BBA in time.

👉 Bottom Line: Section 194P offers a sweet shortcut, but only for very specific, simple financial situations.

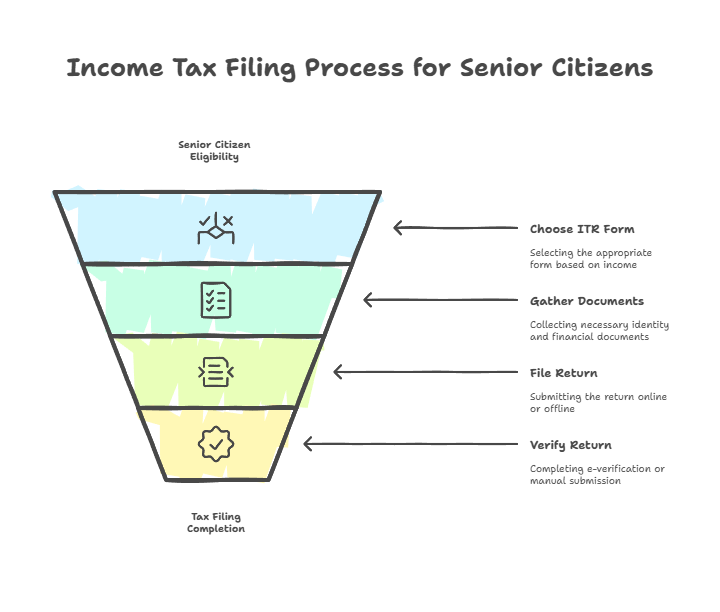

Step-by-Step ITR Filing Process for Senior Citizens

For senior citizens not eligible under Section 194P (which is most of you!), filing ITR is still straightforward, if you follow this process:

1. Choose the Right ITR Form

Selecting the correct ITR form is step one; it determines what income types you can report.

ITR Form | Suitable For | Key Features |

ITR-1 (Sahaj) | Salary/Pension income, one house property, other sources (interest, dividends), total income ≤ ₹50 lakh | Most common for retirees with simple income |

ITR-2 | Income > ₹50 lakh, multiple house properties, capital gains, foreign assets | For those with slightly complex finances |

ITR-3 | Business or professional income | For retirees running a small business |

ITR-4 (Sugam) | Presumptive income under Section 44AD, 44ADA, 44AE | Simplified for small businesses & professionals |

📝 Pro Tip: Most pensioners and retirees fall under ITR-1 or ITR-2.

2. Documents Checklist: What You’ll Need

Before filing, keep these documents handy:

✅ Identity & Tax Documents

- PAN card

- Aadhaar card

- Form 16 (if applicable)

✅ Financial Statements

- Bank statements (savings + FDs + RDs)

- Pension slips

- Form 26AS

- Annual Information Statement (AIS)

✅ Investment Proofs (for deductions)

- Life insurance premium receipts

- Health insurance (Section 80D)

- ELSS, PPF, NSC, NPS contributions

- Medical expenditure receipts (if applicable under 80DDB)

✅ Other Documents

- Rent receipts (if claiming HRA)

- Donation receipts (Section 80G)

3. Filing Methods Explained

A. Online Filing (E-Filing Portal Walkthrough)

1️⃣ Visit: Income Tax e-Filing Portal

2️⃣ Login using PAN/Aadhaar & password.

3️⃣ Select ‘File Income Tax Return’ → relevant AY → type of filing → applicable ITR form.

4️⃣ Pre-filled details (income, TDS, interest, deductions) will auto-populate via Form 26AS & AIS.

5️⃣ Verify details. Enter missing information if any.

6️⃣ Claim deductions under Chapter VI-A.

7️⃣ Validate & compute total tax liability.

8️⃣ Pay any balance tax due.

9️⃣ Submit the return.

🔟 E-Verify instantly via:

- Aadhaar OTP

- Net Banking

- Bank Account EVC

- Aadhaar OTP

🕰 Deadline: July 31st of the assessment year.

B. Offline Filing (Super Senior Citizens 80+)

- If you’re 80 years or older, you can still opt for paper filing.

- Download ITR-1 or ITR-4 forms from the Income Tax portal.

- Manually fill, attach documents, and submit to the local Income Tax Office.

- Retain the acknowledgement copy for your records.

✅ No digital signature or e-verification required.

Conclusion: Simplifying Compliance While Maximizing Tax Savings

Let’s recap what we’ve just decoded:

✅ Senior citizens enjoy special benefits — higher exemption limits, exclusive deductions like 80TTB, no advance tax, and even full ITR exemption for eligible super seniors under Section 194P.

✅ Choosing the correct ITR form is critical — ITR-1 for most retirees, ITR-2 or others if you have additional income streams.

✅ Offline filing is still allowed for super seniors (80+), offering convenience for those less tech-savvy.

✅ Documentation matters — pension slips, interest certificates, Form 26AS, AIS, and proof of deductions should be ready before you file.

Why Timely Filing Matters — Especially for Senior Citizens

⏳ Timely filing isn’t just about avoiding penalties — it’s about:

- Ensuring your rightful refunds are credited faster.

- Reducing the stress of a last-minute rush.

- Keeping your financial records clean for future loan or visa requirements.

- Avoiding interest under Sections 234A, 234B, and 234C.

👉 Deadline to remember: July 31 of the assessment year.

Final Compliance Tips to Make Filing Stress-Free

🔎 Cross-check Form 26AS & AIS to avoid any mismatches.

📝 Use Form 12BBA if eligible for Section 194P exemption.

🧾 Keep physical copies of key documents for 6 years for audit safety.

🔒 Verify ITR instantly using Aadhaar OTP or net banking to close the loop.

🤝 When in doubt, consult a tax professional — especially if your income situation has changed.

🌟 Bottom Line:

The Indian tax system offers genuine relief to senior citizens, but only if you file smart, file early, and claim every benefit you’re entitled to. A little preparation now can mean smoother finances and bigger savings later.

Frequently Asked Questions

Q1. Who can skip filing ITR?

👉 Only certain senior citizens can skip filing, and that too under very specific conditions:

- You’re 75 years or older.

- You’re a resident Indian.

- Your only income is pension + interest (from the same specified bank).

- You’ve submitted Form 12BBA to your bank.

If you don’t meet all these, you must file your ITR like everyone else.

Q2. Can super seniors (80+) file offline?

✅ Yes!

Super senior citizens, i.e., those aged 80 and above, still have the privilege of paper filing. They can submit:

- ITR-1 or ITR-4

- In physical format

- Directly at the Income Tax office

No digital signatures. No e-verification. Good old-fashioned paper and pen still work here.

Q3. What if excess TDS is deducted?

If your bank or pension provider deducts more TDS than necessary (which happens often), don’t worry:

- File your ITR as usual.

- Declare actual income and deductions.

- The excess tax paid will be calculated as a refund.

- After processing, the Income Tax Department will credit the refund directly to your bank account.

💡 Pro Tip: Always cross-check Form 26AS and AIS to ensure all tax credits are accurately reflected before filing.

Q4. How to claim a refund if eligible?

👉 Filing an accurate ITR is the only way to claim your refund.

Once filed:

- Refund is processed automatically.

- Credit is issued directly to your bank account (linked to your PAN).

- Ensure your bank account is validated on the Income Tax portal to avoid delays.

Q5. Is Form 12BBA mandatory?

✅ Yes, but only for those opting for exemption under Section 194P.

If you qualify (75+, only pension + interest income from same bank):

- Form 12BBA is your declaration.

- Without it, your bank cannot compute tax, and you must file your ITR manually.

For everyone else, no need for Form 12BBA.